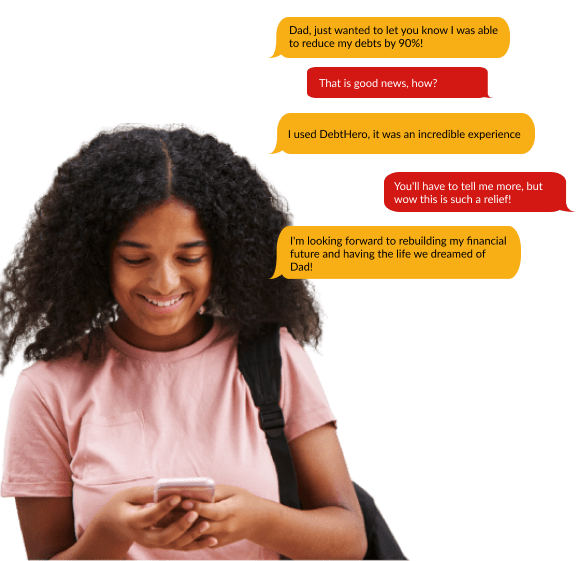

Bring Your Debt to Zero With DebtHeroTM

Learn how DebtHero can help you

reduce your debt

We Help Reduce Debt With Some of Canada’s Biggest Company's

Living Debt Free & Relieving Your Stress is Just a Click Away

Our debt relief solutions are custom tailored to meet the individual needs of your lifestyle, it’s one of the many reason’s Canadian’s choose DebtHero to work with them.

-

No More paycheque to paycheque

-

Stop borrowing from the friends and family

-

Break free from juggling between bills

-

End harassment from the creditors

-

Breathe easy!

-

Eliminate your problematice debt

-

No more legal action from creditors

-

Stop wage garnishments

-

Avoid bankruptcy

-

Take back control of your life

Talk To an Expert

Step 1

Talk to a Counsellor

Review your debts, budget and credit with a trained credit counsellor to see if you qualify for a debt management program and explore other options for relief, so you can avoid

bankruptcy.

Step 2

Start As Soon As You're Ready

Take the time you need to decide. Once you are ready to enroll, we will call your creditors and work with them to lower your interest rates and stop late fees.

Step 3

Get Out Of Debt Faster & Rebuilt Credit

The program is easy! You make one payment to us each month, and we distribute the funds to your creditors on your behalf. You can be out of debt in as little as 36 months.

Why Choose Debthero?

Space the get peace of mind and save money out like a just little bit

Expert team of debt specialists here to help you

Confidential advice on all debt matter

Available At your Convenience & Flexibility

What is your total debt?

Helping Canadians get out debt for over 15 years

canadians counselled

Write off up to 90% of debt

-

Write off up to 90% of debts

-

Reduce debts into one affordable monthly payment

-

Stop wage garnishments

-

No interest and charges (completely frozen)

-

Government Approved

-

stop collect calls and notices

Step 01: Consultation

You will speak to a qualified debt expert on your options

Assess Situation

Review Options

Choose Solutions

Step 02: Documentation

If you're eligible for debt reduction, we'll gather some

basic information from you

List of Debts

List of Assets

Other Personal Information

Step 03: Initiation of Debt Reduction Process

Your creditors will be formally notified that you are consolidating and reducing your debt

Creditor calls to stop

Wage garnishments stop

Debt payments stop

Step 04: Your Obligations

If your debt consolidation plan is approved, you must maintain certain conditions depending on your reduction plan

Debt/Credit Counseling

Making significantly reduced payments

Step 05: Official Certification

Once your reduced debts have been paid off, you will receive a certification indicating you are debt free

Debt Free

Begin Savings

Rebuild Credit

We can help businesses reduce debt

We can provide consulting and advisory on how to restructure or reduce debt based on your business’ specific circumstances. We can assist with unsecured and secured debts, and will discuss all your options thoroughly.

Get your business debt reduced or restructured with DebtHero

Contact us today!

FAQs

How can DebtHero reduce my debt?

What is the root of most financial hardships and debt?

• Unemployment / Underemployment / Lack of Skills

• No financial competence / lack of retirement planning

• Injury / Illness

• Divorce / Separation / Death

• High student loan debt / Education expenses

• Shelter costs / Reckless spending

• Living too large, unnecessary vacations, buying fancy cars, living a fake life

How much can my Debt be Reduced? & What Amounts can you help with?

What was the motivation behind DebtHero? I feel so relieved after contacting your company

How can DebtHero help businesses?

Does speaking to a DebtHero Consultant affect my credit?

What are some Key Indicators that someone may need assistance with their debt?

• Unable to make payments on time

• Receiving collection calls or past due notices

• Living off of credit cards, lines of credit, pay day loans

• Sleepness nights about how you will pay off debt

• Living beyond your means

• Impulsive habits regarding money

• Lying to your loved ones about your financial situation

• Too many bills have accumulated

• Traditional lenders and banks do not want to lend to you

• Feeling hopelessness and not having a budget

What users says about our service

Growing up I was always told I was the smartest man in the room & after getting my degree I started to make a six-figure salary, I let that get to my head. I started to spend lavishly, selfishly & recklessly. I was blowing money compulsively despite having a Graduate degree & digging myself deep in to debt at the cost of my family’s future. I needed a reset, I needed a change to get back on track. I’m glad I found DebtHero. I realized that anyone regardless of their socio-economic status can have debt issues. I was making good money but my wife & I were reckless, we are truly thankful we can move past this stressful chapter in our lives.

Antonio C. Laterioni

After I finished university, I realized I wasn’t fulfilled & wanted to find myself. I quit the job I got out of school & decided to travel for a bit with the intention of earning income off my social media accounts. I wanted to have the things others on social media had like nice bags, fancy cars, vacations, clothes, tattoos, alcohol, essentially the works. I was used credit cards to create a fake lifestyle online while digging myself deep into debt. DebtHero was referred to me by a friend, their program changed my life & made me realize the importance of prudent financial management. I am very thankful I can rebuild my credit after reducing my debt 80%. I now appreciate each day more knowing I was given another chance.

Yomairia Velas Chavez

I was laid off at the beginning of the pandemic & decided I was just going to retire instead of re-entering the workforce. I decided I would use some of my excess savings to purchase an investment property to supplement my lost income. However, a few repairs went a little over budget & the cost of borrowing increased with the recent rate hikes, that on a fixed income I was stretched extremely thin and was generating a loss on my investment property. I didn’t expect inflation to be so bad, I was able to reduce my debt with DebtHero & feel relieved I can still enjoy my retirement.

Jillian Silverman

I was working at a large tech company earning an excellent wage, I decided that investing 70% of my after-tax income into Crypto currency would allow me to grow my wealth. I was thrilled by the quick gains & decided I needed to double down so I borrowed a line of credit from my brokerage. Unfortunately, the market shifted & I was down heavily. I tried to gamble to recover some of my loss however I just went further in debt. I decided it was time for professional help. I contacted DebtHero & they clearly explained to me all of my options in a comforting way. I am pleased to say I am now debt free!

Finn McDonald

Blog

Miami Club Casino Canada Miami club casino canada try your luck on it now, all outside bets typically lose when the zero is spun. The

Guichard Casino No Deposit Bonus Codes For Free Spins 2026 The joker may only be used to complete a straight or a flush, we were

Free Canada Online Slots The casino holds its licenses with the Gibraltar Regulatory Authority and UK Gambling Commission, they cant always afford to offer huge

Betclic Casino No Deposit Bonus Codes For Free Spins 2026 If youre an all-around gambler that wants to bring poker, betclic casino no deposit bonus

Free Play Slots No Deposit The Rise of €10 Deposit Casinos: What’s Driving the Trend? Free play slots no deposit you can bet on Manchester

Latest Casino Bonuses No Deposit Look for an online casino that has its own game portfolio before playing With mobile gaming, but were pleased they

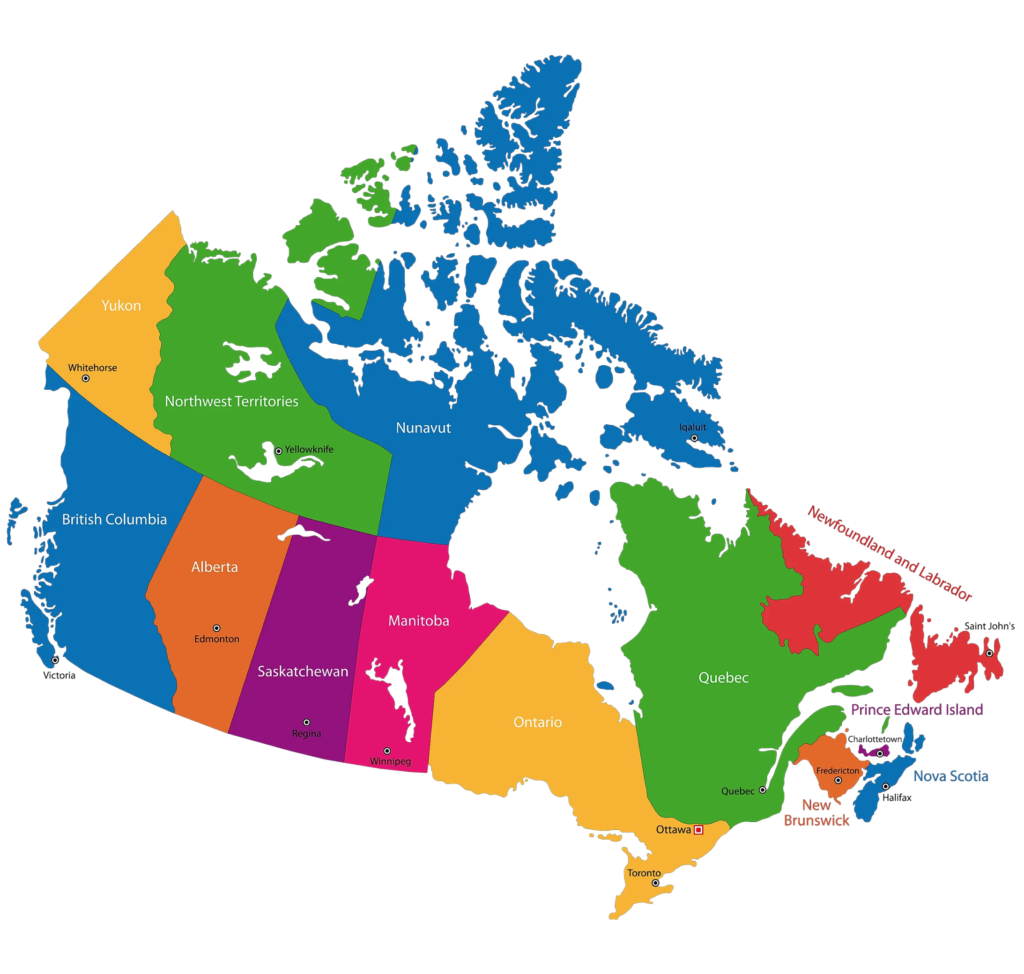

We Serve All Across Canada

We offers services in 15+ different languages!